Last night’s Federal Budget contained the most significant changes to capital gains tax, negative gearing and trust taxation in some time.

Here is a summary of three core changes that matter most for the assets and structures you own and hold.

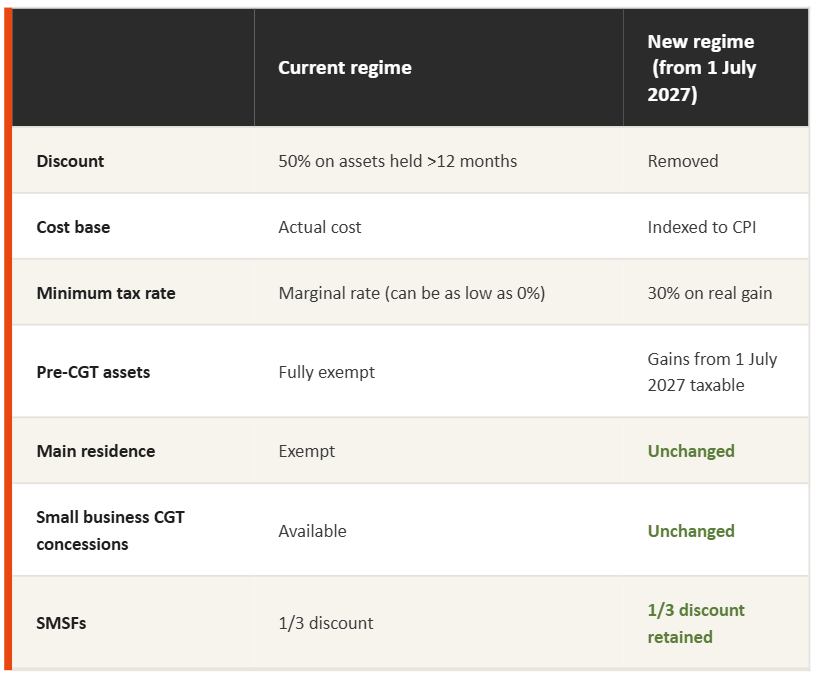

Capital Gains Tax

Effective 1 July 2027

The 50% CGT discount for individuals, trusts and partnerships is being replaced by two things working together: cost base indexation (so only the inflation-linked adjusted gain is taxed) and a 30% minimum tax rate on net capital gains.

How existing assets are treated: The 50% discount applies in full to gains accrued up to 30 June 2027. Only growth from 1 July 2027 onwards falls under the new regime. The value of each asset at 1 July 2027 is established either by formal valuation or by an ATO-prescribed apportionment formula based on holding period and growth rate.

CGT regime comparison

Current rules vs the new regime from 1 July 2027

Negative Gearing

Effective 1 July 2027

Negative gearing on residential property will be restricted to new builds. Commercial property and shares are unaffected.

Properties held at 7:30pm AEST on 12 May 2026 are fully grandfathered. Existing arrangements continue until sale.

Properties purchased between Budget night and 30 June 2027 may be negatively geared during this period only.

From 1 July 2027, losses on established property purchased after Budget night can only offset other residential property income (rent or capital gains), with carry-forward available, but not wages or other income.

SMSFs and most widely held trusts are excluded from these restrictions.

Discretionary Trusts

Effective 1 July 2028

A minimum 30% tax rate will apply to discretionary trust income, paid by the trustee. Beneficiaries (other than corporate beneficiaries) receive a non-refundable tax credit, so the impact falls on beneficiaries with marginal rates below 30%, i.e. those with taxable income under $45,000.

Excluded structures: fixed and widely held trusts, complying super funds, special disability trusts, deceased estates, and charitable trusts.

Excluded income types: primary production income, income from existing testamentary discretionary trusts, certain income to vulnerable minors, and amounts subject to non-resident withholding tax.

Three-year rollover relief from 1 July 2027 to 30 June 2030 to support restructuring out of discretionary trusts into other entities (e.g. companies, fixed trusts) without triggering CGT.

What this means

The changes favour longer-held, lower growth assets and reduce the tax efficiency of leveraged residential property and high-growth holdings inside discretionary trusts.

We will be working through each of these in your next review and will tailor the response to your specific holdings, structure and timeline.

Legislation is yet to be drafted and detail will continue to emerge through Senate negotiations. We will be sure to keep you updated.

Stay informed with our team’s exclusive complimentary market insights and strategic updates. Click this link to join our distribution list.