April was a tale of two markets. Offshore equities staged one of the strongest risk-on rallies of the cycle, led by a decisive rotation back into AI and the broader technology supply chain – the S&P 500 and Nasdaq notched fresh highs, and emerging Asia surged on Taiwan and Korea-led semiconductor strength. The ASX 200, by contrast, faded meaningfully into month-end as the index's cyclical and defensive tilt collided with renewed domestic inflation pressure and the prospect of further RBA tightening. Geopolitical stress remained acute – the Strait of Hormuz disruption persists and Brent pushed back above US$110/bbl – yet markets looked through it on improved earnings momentum and renewed AI capex enthusiasm.

Domestic

ASX 200 Lags the Global Bounce: The ASX 200 closed April with a modest gain at 8,665.8, retracing meaningfully from a mid-month high. Materials and Financials drove the upside, with BHP, Macquarie, CBA and Goodman the standout contributors. Health Care was the largest detractor, dragged by CSL and Cochlear; Information Technology rallied sharply (NextDC the standout) but off a small base. Small caps modestly outperformed large.

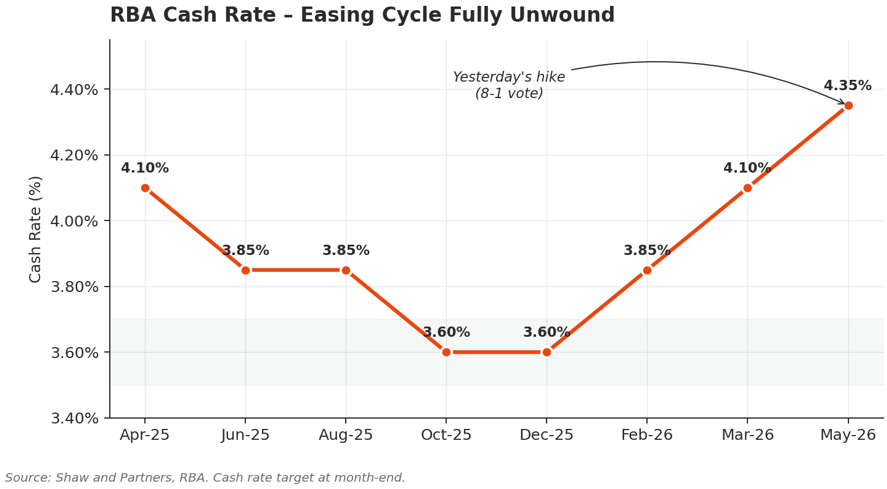

RBA Hikes to 4.35% – Third Consecutive Move: At yesterday's May meeting the RBA lifted the cash rate by 25bps to 4.35% in a split 8-1 decision, fully unwinding the 2025 easing cycle. The Board flagged that the Iran-related oil shock has "complicated things immensely," upgraded near-term inflation forecasts, and warned of "second-round effects" – leaving the door open to further tightening. Westpac is forecasting two further hikes; markets are now pricing additional risk into June and August.

Inflation Re-accelerating: Headline CPI hit 4.6% YoY in March, with trimmed mean still sticky in the low 3s. Higher energy prices linked to the Strait of Hormuz disruption are flowing through fuel, freight and input costs. The AU 10Y bond yield drifted higher to ~5.06% in April, with FY27/28 earnings forecasts now embedding higher-for-longer rates.

Earnings Inflection – First Downgrade in the Cycle: FY26e EPS growth was revised lower for the first time in the cycle, largely reflecting Energy re-profiling (back-ended into FY27). Health Care, Software & Services and Pharma/Biotech led the downgrades. Forward P/E re-rated modestly higher to ~16.8x (above the 10Y average) on the softer earnings pulse, leaving valuation support thinner heading into August reporting.

AUD Strength a Partial Offset: AUD/USD rallied through the month on broad USD weakness and stronger commodity terms-of-trade, narrowing Australia's relative underperformance vs global peers in USD terms. Iron ore held firm; copper and energy commodities were the clear bright spot, with thermal coal extending its strong recent run.

Federal Budget Next Tuesday (12 May): Macro focus will be less on the headline deficit – where the cyclical backdrop is improving – and more on how revenue uplift is deployed, particularly through government spending growth and net policy stimulus. Any meaningful fiscal expansion would complicate the RBA's task and could pressure long bonds further.

International

AI Trade Reasserts Global Leadership: Global equities staged a powerful risk-on rally led by AI-leveraged names. The S&P 500 led developed markets, the Philadelphia Semiconductor Index surged ~40%, and MSCI EM was the standout regional index – powered by extraordinary gains in Taiwan and South Korea, the deepest beneficiaries of the AI semiconductor supply chain. Growth decisively outperformed Value globally.Fed Holds at 3.50-3.75% – Sharp Internal Divide: The FOMC held rates unchanged on 29 April for a third straight meeting, but the 8-4 dissent was the most since October 1992 – one Governor wanting cuts and three opposing the statement's easing bias. Markets are now pricing no changes through 2026 and well into 2027. Powell's chairmanship ends 15 May with Kevin Warsh likely confirmed as successor; first opportunity for a policy shift is the 16-17 June FOMC.

US Earnings Season Strong: Roughly two-thirds of S&P 500 by market cap have reported, with EPS growth tracking comfortably double-digits. Beat rates are running well above the historical average and earnings are coming in materially ahead of expectations – though heavily skewed by hyperscaler investment gains. The breadth of the beat plus the AI capex cycle drove sentiment.

Energy Crisis Persists: The Strait of Hormuz remains severely disrupted with intermittent ceasefire attempts breaking down. Brent closed April well above US$110/bbl despite a small monthly pullback, and thermal coal extended its sharp recent run. Higher energy prices are weighing on global government bonds (UK Gilts and JGBs both lower, with 10Y JGB at the highest level since 1997) and complicating central bank decisions globally.

Europe Lags on Energy Drag: Europe ex-UK posted a soft month as early ceasefire optimism faded and the Eurozone PMI printed back in contraction. UK FTSE All-Share was the clear DM laggard, with UK CPI rising and markets now pricing two further BoE hikes by year-end. Japan's Topix added a modest gain, constrained by limited direct AI exposure.

USD Weakens Broadly: The DXY fell through the month, with EUR/USD and AUD/USD both higher. The combination of a softer dollar and risk-on sentiment supported emerging market debt, which outperformed within credit. Gold consolidated after a strong run.

Looking Ahead

Australian Earnings Risk Re-emerges: With FY26 forecasts beginning to be cut for the first time in this cycle and the index trading above its 5Y and 10Y average multiple, valuation support is now thinner. Sector dispersion is increasing beneath the index, and confession season ahead of August reporting could drive further volatility – particularly across Health Care, Staples and discretionary cyclicals.

Stagflation Risk Skewing Domestic Outlook: RBA Deputy Governor Hauser has warned of the "nightmare" scenario: inflation accelerating even as growth weakens. With the cash rate now back at the prior cycle peak (4.35%) and household balance sheets under pressure, the trade-off is sharpening. Defensive earnings, infrastructure and quality balance-sheet exposures look better positioned than rate-sensitive cyclicals.

AI Capex Cycle vs Concentration Risk: The April rally was overwhelmingly driven by AI-leveraged technology and semiconductor supply chain names. While the earnings backdrop remains supportive, the breadth question is becoming more acute. Diversification across geographies and away from the most crowded AI exposures looks increasingly prudent into a concentrated, two-sided risk environment.

Energy as the Swing Factor: A timely re-opening of the Strait of Hormuz could see oil fall sharply, easing inflation pressure and allowing rate expectations to soften globally. A continuation – or escalation – of the blockade would entrench inflation and dampen activity simultaneously. Energy and Materials remain the cleanest expressions of the upside scenario; long-duration assets benefit from the downside.

Fed Leadership Transition: Powell's chairmanship ends 15 May. Warsh's confirmation and his June FOMC debut will be a key signal for how monetary policy is communicated and prioritised in the post-Powell era. Any meaningful dovish shift could drive USD weakness and support EM and gold.

Potential Catalyst Watch:

Federal Budget (12 May)

April Labour Force release (15 May)

Q1 Wage Price Index (14 May)

Q1 CPI confirmation and RBA SoMP detail

Senate vote on Kevin Warsh as Fed Chair (week of 11 May)

Strait of Hormuz / Middle East ceasefire developments

“Experience is what you got when you didn't get what you wanted.” — Howard Marks

If you'd like to discuss how these themes may apply to your portfolio or investment strategy, feel free to get in touch.