AI has dominated global markets for three years now, but the conversation in Australia usually starts with what we don't have – no Nvidia, no hyperscalers, a tech sector worth a few per cent of the index. We think that misses the point. Australia's AI opportunity is coming through the real economy – data centres, electricity, critical minerals, construction and capital markets – and those are the things this market has in abundance.

1. The biggest investment cycle since the mining boom

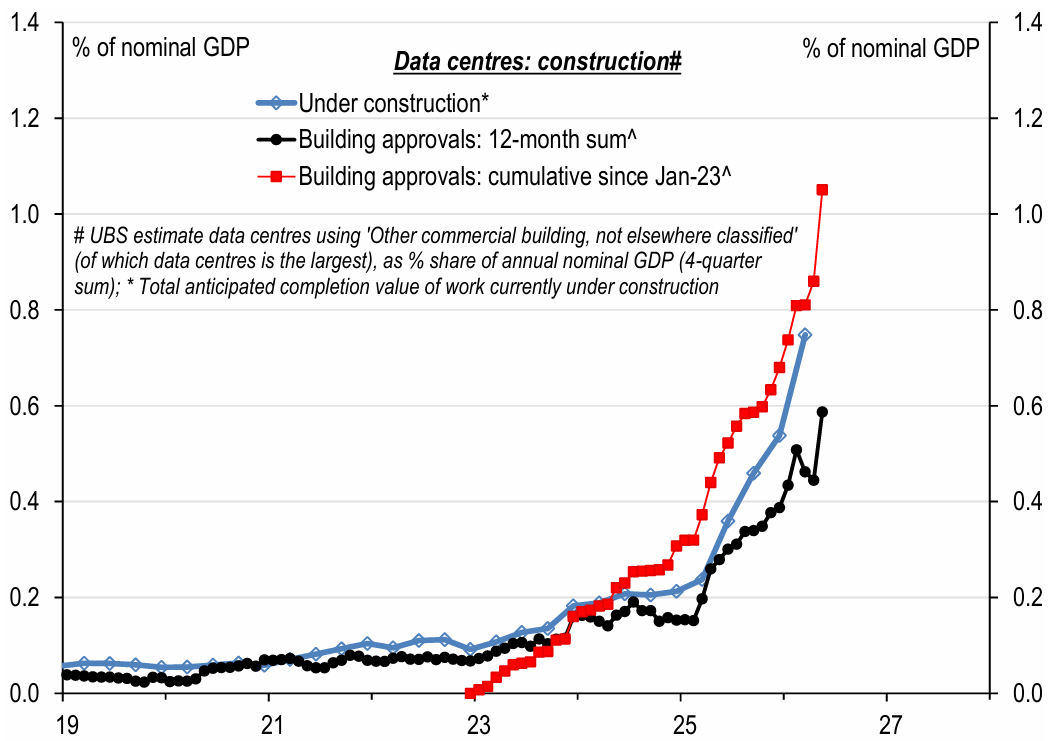

AI-related investment in Australia has roughly tripled over the past year. There is now about A$21.6bn of data centres under construction – around ¾ of a percent of GDP – and with building approvals still accelerating, UBS sees the peak heading towards 2% of GDP over the next year or two. That makes this the most significant investment cycle since the mining boom, even if it won't reach the ~7% of GDP mining hit in 2011.

Two things follow for portfolios. Near term, the spend is inflationary – it doesn't respond to the cash rate, which is partly why we expect the RBA to hike to 4.60% in August. Longer term, the productivity benefit should pull the other way. And for all the headlines, government research has found no real evidence yet of AI disrupting the jobs market. This is a capex story before it is a jobs story.

Figure 1: Data centres under construction in Q1-26 already spiked to ~$21.6bn

Source: UBS, ABS, Macrobond

2. What history tells us about disruption scares

Markets have a mixed record of pricing new technology threats, and the ASX offers three instructive precedents:

The internet vs traditional media: the threat was real – classifieds moved online for good and free-to-air TV shrank to near-irrelevance. But REA Group lost ~90% of its value in the dot-com bust before becoming one of the market's great compounders. Investors were right about the shift, wrong on timing.

Amazon vs local retail: priced in 2017 as an existential threat to JB Hi-Fi, Harvey Norman and Super Retail. The launch underwhelmed, incumbents held their ground, and the de-rated quality names re-rated strongly.

GLP-1s vs ResMed: weight-loss drugs were priced as demand destruction, knocking 25–36% off the stock through 2023. Management now calls them a tailwind, and the shares recovered as earnings held up.

The pattern is consistent: disruption themes tend to be directionally right, poorly timed and indiscriminately priced. We think much of the AI trend is structural, and that a cyclical overshoot is likely too. That creates opportunity on both sides – in the enablers, and in quality businesses oversold on the threat.

3. A market built on physical strengths

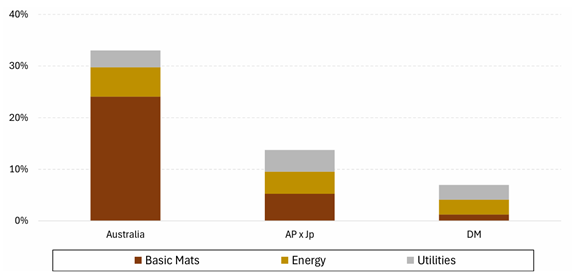

The lack of big tech has cost the ASX dearly over the past year – up just 3% against 20% for the S&P 500 and 22% for Asia. But the same composition is starting to look like a strength. Minerals and energy can't be produced by AI; they are what AI is built on. The heavy weighting of materials, energy and utilities makes this market something of a safe haven if the theme wobbles.

The market has already voted. The capital-light software and platform names that led 2023–24 have de-rated hard – UBS's basket of ASX 'intangibles' is down ~35% in a year, with Xero and WiseTech more than halving – while asset-heavy names have outperformed since mid-2025. We think of the local exposure as a value chain: the data centre developers and operators at the front (Goodman, NextDC, DigiCo, Megaport), the utilities, miners and servicing names behind them (AGL, Origin, BHP, Sims), and capital markets and industrial services behind those (Macquarie, Worley, Ventia).

Figure 2: Weights of Basic Materials, Energy & Utilities within equity market

Source: UBS, LSEG

4. Who's best placed – and what's already priced

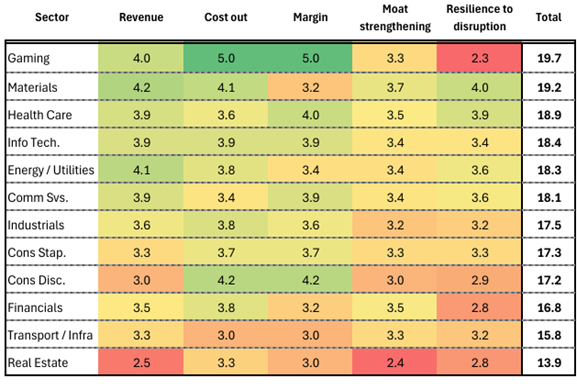

UBS scored every company it covers on five dimensions – revenue, cost-out, margin, moat and resilience to disruption – under a moderate adoption scenario over the next three years. Gaming and materials lead; real estate ranks last:

Source: UBS

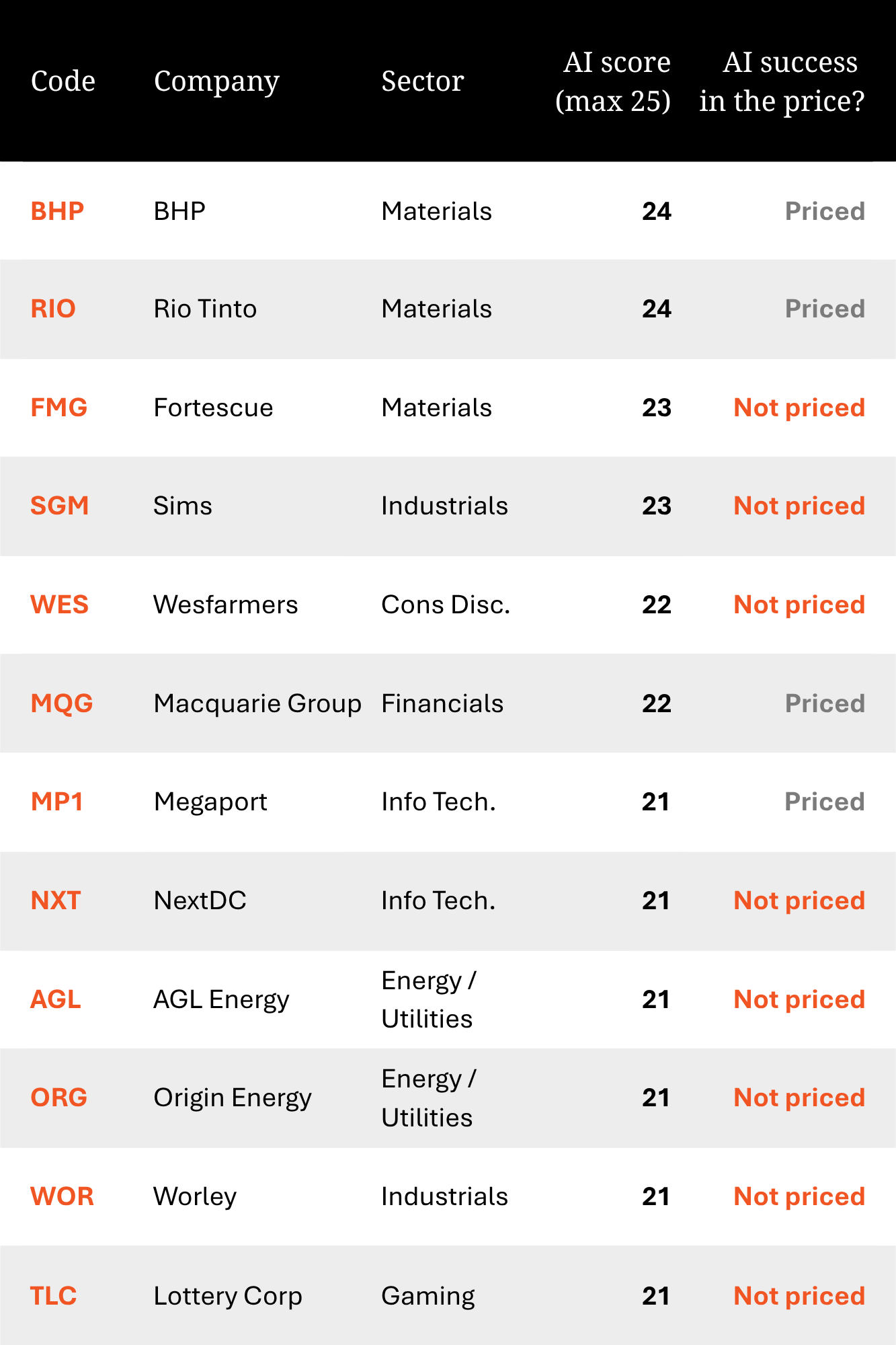

What struck us is how little of this is in the price. The most 'AI-ready' stocks do already trade at a 10-point PE premium and an 80% relative ROE premium to their less-favoured peers. But across its entire coverage, only six companies are determined to be fully priced for AI success – CBA, Macquarie, BHP, Rio Tinto, Technology One and Megaport. If even moderate adoption plays out, most of the ASX 200 has upside risk to earnings.

5. Where we see the opportunity

We approach it in two layers. The first is conviction on the highest scorers, led by the big miners. This is not narrative: BHP's AI-driven plant control has saved 3 billion litres of water and 118GWh of energy at Escondida since FY22, and around 90% of Rio Tinto's Pilbara haul fleet is autonomous. These are proprietary datasets and workflows smaller peers can't replicate, and the theme also underpins demand for the copper, lithium and rare earths producers further down the curve.

We approach it in two layers. The first is conviction on the highest scorers, led by the big miners. This is not narrative: BHP's AI-driven plant control has saved 3 billion litres of water and 118GWh of energy at Escondida since FY22, and around 90% of Rio Tinto's Pilbara haul fleet is autonomous. These are proprietary datasets and workflows smaller peers can't replicate, and the theme also underpins demand for the copper, lithium and rare earths producers further down the curve.

Source: UBS

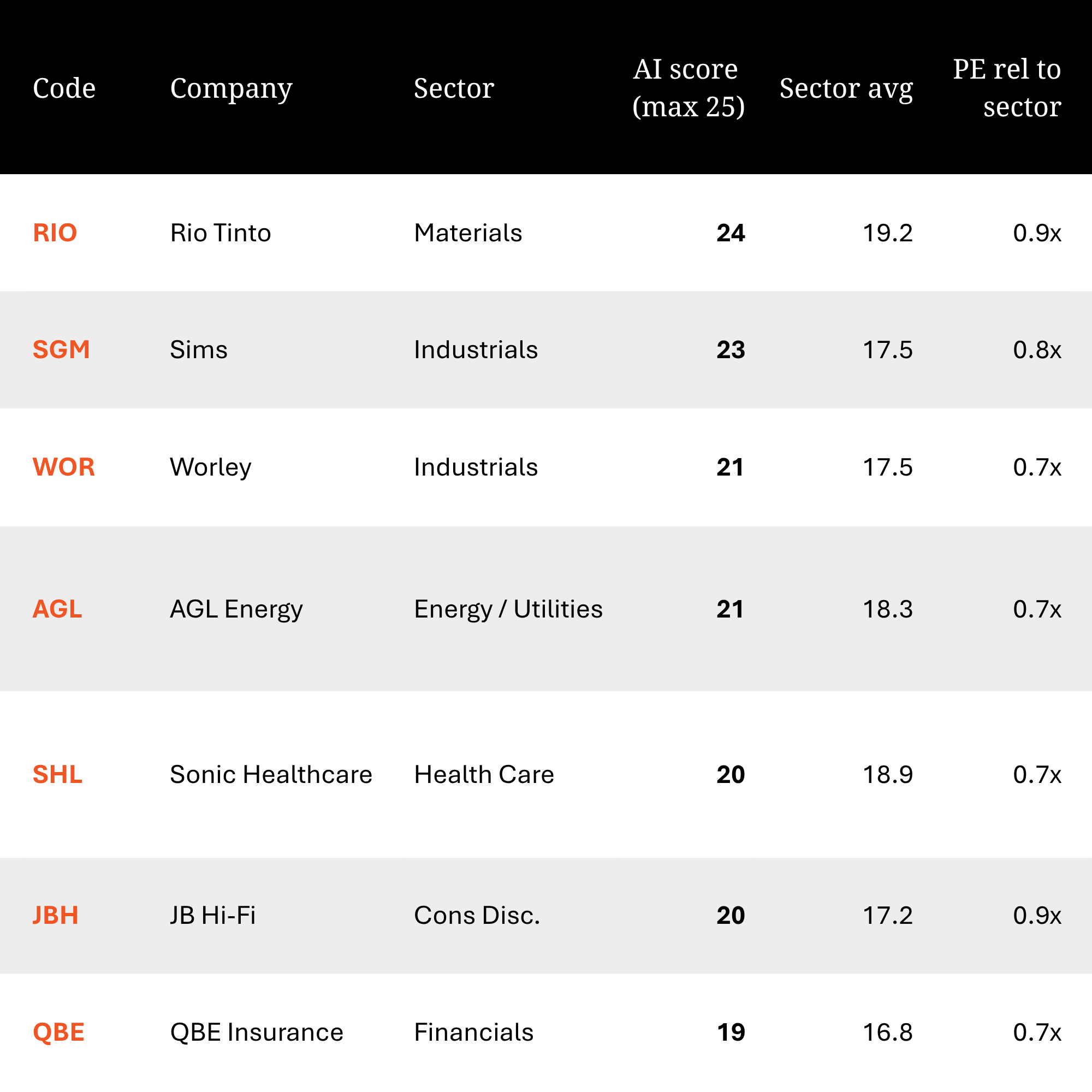

The second layer is value. Most of the names above already trade on premium ratings – the more interesting screen is the relative AI winners still priced at a discount to their sector:

Source: UBS

Rio Tinto stands out – the equal-highest AI score in the market, still below its sector multiple. Sims gives you the theme twice over, through memory chip recycling and copper volumes. Worley is a direct play on the data centre and power engineering build-out, and AGL pairs the electricity demand story with cost-out potential at ~0.7x its sector.

Our view. This theme rewards selectivity, not a blanket tech trade. We see the most durable exposure in the miners, power and infrastructure names supplying the build-out – where AI is already proven in the operations – and in quality operators using it to widen existing moats, particularly where that isn't yet in the price. The indiscriminate sell-off in quality capital-light names also looks a lot like past disruption scares; for patient investors there is opportunity on that side of the trade too.

If you'd like to talk about how any of this applies to your portfolio, or would like the full research, get in touch.