What’s Happening

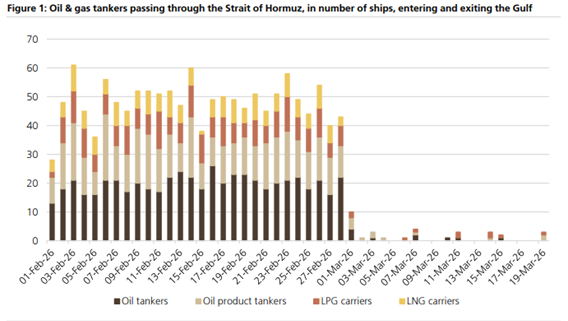

We are now 20 days into the Strait of Hormuz closure. Tanker traffic – normally around 50 oil and gas vessels per day – has collapsed to near zero. The average for March to date is below 2 vessels per day, compared to nearly 50 throughout February.

Source: UBS Evidence Lab, S&P Global Market Intelligence

Over the weekend, President Trump issued a 48-hour ultimatum to Iran: re-open the Strait or face strikes on Iranian power infrastructure. The potential consequences are significant, neutralising Iran’s electrical grid would affect oil production, water systems, petrochemical manufacturing, hospitals, and telecommunications. Iran’s parliamentary speaker has responded by declaring all regional energy infrastructure as legitimate targets in the event of such strikes.

Both the S&P 500 and ASX 200 are down more than 8% from recent highs. Bond yields continue to rise. With this level of uncertainty, forced liquidation and risk-off sentiment remain the dominant forces in the short term, and the sell-off has been broad and indiscriminate — quality businesses with little or no energy exposure have been dragged down alongside those directly impacted.

Energy Repricing

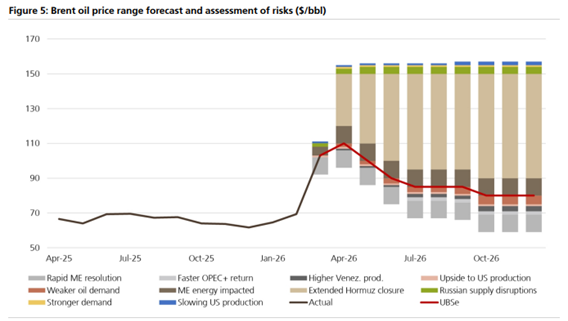

UBS has upgraded Brent crude forecasts by US$10–20/bbl over the next two years. Their 2Q26 estimate now sits at US$100/bbl, though the long-term CY28 figure remains at US$75/bbl. The working assumption being that the disruption is ultimately temporary. However, they also acknowledges there could now be an elevated risk premium embedded in markets that persists even after a resolution, resulting in higher medium-to-long term prices than previously expected.

The more dramatic move has been in natural gas. Following the attack on Qatari LNG facilities, JKM spot prices have doubled from around US$12–13/mmbtu to US$26/mmbtu. This is a material positive for Australian LNG producers – particularly Woodside and Santos, who sell the majority of their LNG into Asia-Pacific markets linked to that benchmark. Higher gas prices also flow through to thermal coal pricing, supporting names like Whitehaven.

Source: DataStream, UBS estimates. Brent price range forecast and assessment of upside/downside risks.

The Inflation Question

One of the key concerns driving the sell-off is the inflationary impact of higher energy prices and what that means for interest rates. We think markets may be over-estimating this risk.

Energy-driven inflation is fundamentally different from demand-driven inflation. Higher energy prices are themselves a brake on consumer spending and economic growth, they are, in a sense, self-correcting. Central banks understand this distinction. Energy inflation does not necessarily require higher rates to rein it in; the price shock itself does much of the work. This is an important nuance that gets lost when headlines are dominated by CPI prints.

Global government bond yields will likely continue to rise until a resolution occurs, and that affects all asset prices. But we would caution against extrapolating the current rate environment as permanent.

Valuation: Where We’ve Seen This Before

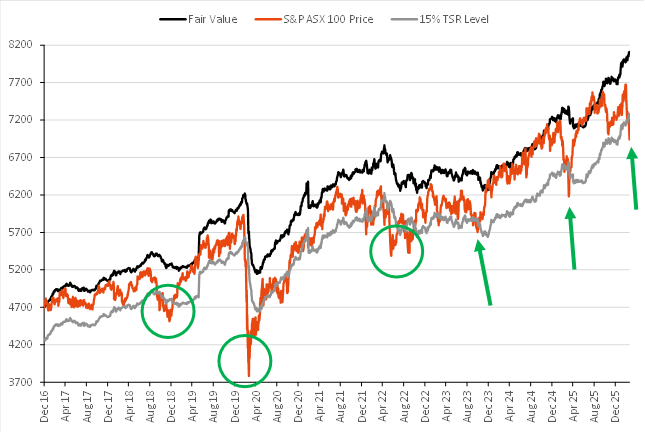

The ASX 100 is now trading at a meaningful discount to consensus fair value. The chart below shows this relationship over the past eight years. Each time the gap has widened to current levels — marked by the green circles (late 2018, COVID, late 2022) — it has proven to be an excellent entry point for investors willing to look through the near-term uncertainty.

S&P/ASX 100 price vs consensus fair value and 15% TSR level. Green circles highlight prior valuation dislocations.

Implied 12-month Total Shareholder Return for the ASX 100: 20.5%.

Based on consensus target prices and dividends, this is an unusually wide gap and reflects the degree of fear currently priced into the market.

Where We See Opportunity

In broad-brush sell-offs like this, many quality companies are indiscriminately sold even if they have limited direct exposure to the underlying shock. That creates opportunities. Below are the sectors and names that stand out to us on both a valuation and quality basis.

Gold: Genesis (GMD), Ramelius (RMS), Northern Star (NST), Newmont (NEM). The recent pull-back in the gold price has opened up attractive valuations, and gold remains a natural hedge against further geopolitical escalation.

Software: WiseTech (WTC), REA Group (REA), Life360 (360), Light & Wonder (LNW), Xero (XRO). The “Saascopalypse” has pushed several structural growth businesses into deep value territory. These are companies with strong recurring revenue profiles now available at cyclical-low multiples.

Healthcare: CSL, Cochlear (COH), Sonic Healthcare (SHL), Telix Pharmaceuticals (TLX). The sector screens well as a defensive play if the conflict extends, and all four names are oversold and cheap relative to their historical trading ranges.

US Industrials: Amcor (AMC), James Hardie (JHX). USD-denominated earnings, heavily sold down, and largely insulated from Middle Eastern energy dynamics.

Real Estate: Dexus (DXS), Mirvac (MGR), Stockland (SGP), Goodman Group (GMG). All appear cheap on a price-to-book basis relative to their 10-year averages and are trading near 52-week lows.

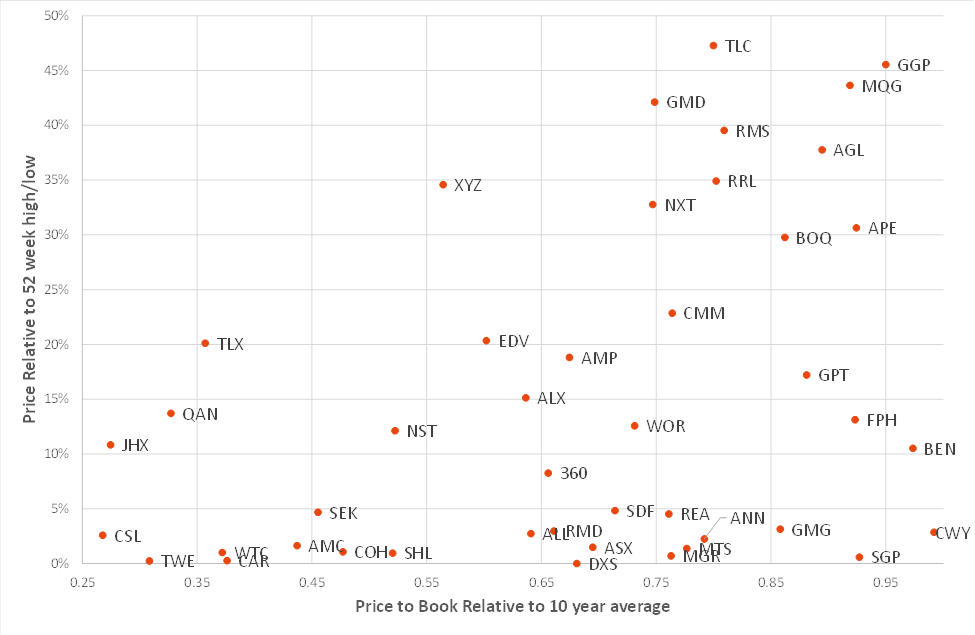

The scatter chart below maps ASX 100 stocks by their price-to-book ratio relative to the 10-year average (x-axis) against their position in the 52-week trading range (y-axis). Stocks in the bottom-left corner are both historically cheap and near their annual lows — these represent the most dislocated opportunities.

ASX 100: Price-to-Book relative to 10yr average vs position in 52-week range. Bottom-left = most dislocated.

How We’re Positioned

We are managing through this dislocation on two fronts. First, tactically increasing energy exposure — on the ASX, that means Woodside, Santos, Beach Energy, and Whitehaven Coal. All have already moved higher but could see further significant upside if elevated energy prices persist. Second, taking advantage of the sell-off in quality names that are now 10–30% cheaper than three weeks ago, despite having limited direct exposure to the energy crisis.

If and when a resolution is reached in the Middle East and the Strait re-opens, markets are likely to refocus quickly on fundamentals – and the fundamentals continue to look attractive. We believe some form of short-term resolution should prevail, which would trigger a near-term rally.

In the meantime, we believe portfolios are currently well positioned for significant longer-term outperformance once bond market intervention inevitably occurs. We continue to make selective adjustments rather than wholesale changes – the core positioning is right for this environment.

If you'd like to discuss how these themes may apply to your portfolio or investment strategy, feel free to get in touch.